Archive for the ‘Newsletter’ Category

CrossleyShear Wealth Management's Media

Make data privacy a priority in 2022

Make data privacy a priority in 2022

As our lives become more digitally integrated, our data becomes more valuable.

Often, data collectors say that the vast amount of information they take in is tightly secured or anonymized before it is packaged and resold. However, MIT researchers discovered in 2018 that individuals could be identified by combining two anonymized data sets covering the same population. A 2019 series from The New York Times went further, exposing the risk to privacy on a massive scale if a major tech firm’s anonymized location data was stolen and cross-referenced to publicly available property records.

As long as consumers’ concerns about privacy remain limited, there is little incentive for companies to cull their data collecting habits. When buying a new smart device such as a phone, tablet or computer or using a new service, look into its commitment to privacy. The market for such devices is growing, but at the moment they tend to be on the premium side of the product spectrum. Expect that to change as this topic gains traction.

In the meantime, here are some best practices to help minimize the amount of your information that data collectors can access.

Turn off personalized ads

Many of the largest ad space sellers, particularly those providing tech services like email and social media, now give the option to depersonalize your advertising experience. They’ll still collect the information, but there are some limits to how specifically targeted the ads can be. This is becoming a battleground topic in the tech industry, as companies that don’t rely on ad sales are finding privacy to be a strong selling point.

Skip the quiz

That silly online quiz to help you determine which fast food mascot you are may be mining serious information about you. Though it’s a bad practice, many online accounts rely on security questions to establish your identity, questions that are easily snuck into online quizzes.

Go digital and shred the rest

Your home or driveway may be advertising your wealth, making your mailbox and your trash a target. Despite the well-publicized thefts of user data in recent years, an online account is in many ways more secure than an unlocked mailbox, and generally less personal. Privacy experts recommend making the switch, and when you do get mail that contains information about your health, finances or family, make sure to shred it before you toss it.

Know what health data is being collected

The Health Insurance Portability and Accountability Act, or HIPAA, protects the information shared with your care provider. There is no similar regulation for health data you share with your fitness device manufacturer. It’s worth your while to make sure you understand what information is being collected and for what purposes. Go into the device settings to see what options you have. The EULA, or end-user license agreement, will have more information if you can read legalese.

Sources: The New York Times; Vox; The Washington Post; Fast Company; Massachusetts Institute of Technology; Consumer Reports; NPR; Goldman Sachs; ZDNet.com

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.

Document shredding and food drive

Document shredding and food drive event

Clean out your cabinets and drawers of those old documents and bring them to be safely shredded, on site, by the professionals of Shred it™ and enjoy some good food and live music!

When: May 21st

Where: Outside of the Merritt Island office 2395 N. Courtenay Parkway

Time: 11:00am-2:00pm

Question please contact karin@crossleyshear.com or call 321-452-0061

Please consider bringing a non-perishable food item for our Food Drive to benefit Harvest Time International

Please Donate

- Low sodium canned vegetables

- Canned meats

- Canned soups

- Boxed oatmeal or grits

- Canola or olive oil

- Peanut butter

- Nuts

- No sugar added fruit cups

- Canned beans

- Granola/Protein bars

- Pasta

- Beans

- Rice

- Dry powdered milk

Raymond James is not affiliated with Harvest Time International or 4th Street Fillin Station

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.

From the Desk of Dale Crossley and Evan Shear

From the Desk of Dale Crossley and Evan Shear

“The stock market is a device to transfer money from the impatient to the patient.”

Warren Buffett

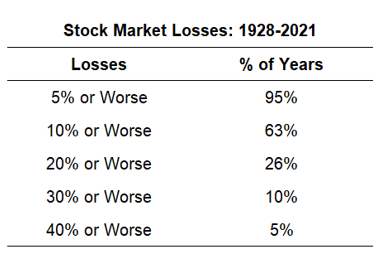

We’re approaching two years since the COVID-19 pandemic began, which as we can all vividly remember, caused very deep wounds on the financial markets. With pandemic stimulus support and liberal monetary policy from the Federal Reserve, the economy largely rebounded and stocks flourished in 2021. Now, we’re ringing in 2022 with the worst market start to a new year since 2016. We’re hearing from many clients who are increasingly concerned that a pullback is in full swing and a market correction (or worse) is on the horizon. Federal Reserve changes are causing concern as they appear necessary to increase interest rates and curb rising inflation. While we all dread market corrections, we inherently know they are inevitable and, as an investor, being both patient and keeping history in perspective helps navigate through these times.

Gaining Reassurance from History

After surviving February and March of 2020 (and others this century), market fluctuations, corrections and, unfortunately, crashes are inescapable. However, in most years since 1928, we only experienced losses of 5% or slightly worse. As a matter of fact, we only experienced losses of 10% or worse in more than half of the years. Despite those fluctuations, long-term investors, who remained patient and invested, and are still very much ahead.

(These averages are skewed a little higher because of all of the crashes throughout the 1930s, but even in more modern times, stock market losses are a regular occurrence. Source: https://awealthofcommonsense.com/2022/01/how-often-should-you-expect-a-stock-market-correction/)

Is it a Pullback, Correction or Bear Market?

- We experience pullbacks in most years, which are market declines of between 5% and less than 10% from a peak.

- A correction is a loss of 10% to less than 20% from a peak. Far from uncommon, we’ve had seven since 2000.

- A bear market is relatively rare and represents a decline of 20% or more from a peak. We’ve only had three since 2000.

Keeping Perspective

As always, we remind our clients that emotional financial decisions are rarely helpful and can actually be devastating. That’s precisely why we developed Voyage, our investment and wealth building process that uses mathematical algorithms, coupled with a methodical, proprietary scoring process. Our models provide disciplined and unemotional “buy” and “sell” signals as fluctuations in the market occur. Based on these signals, client assets are then moved between stock, bond, sector, money market mutual funds and exchange-traded funds. We stress patience and riding out pullbacks, corrections and bear markets. As you can see, history tells us they always rebound.

To learn more, click here to read our article “How Do Rising Interest Rates Affect Stocks.” We’ve also provided a short video recapping article.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.

There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. All opinions are as of this date and are subject to change without notice. Past performance is not a guarantee of future results.

Are Your Important Documents Secure and Accessible?

Are Your Important Documents Secure and Accessible?

Keep your financial life organized with a thoughtful combination of digital and physical storage solutions.

Pop quiz: In an emergency, could your loves ones find your current will and power of attorney? If you had to evacuate your home, could you quickly get your hands on your passport, deeds and keepsakes? Are your documents in a watertight, fireproof safe, or scattered around unprotected?

It’s not enough to have the right documents – it’s also crucial to have them updated, neatly stored and accessible. Read on for five tips that can help you keep important files safe and handy.

Equip yourself for digital success

If you’d like to have a secure and organized system for paper, a scanner and a shredder are a must. Think you might need that document, but you can’t fit another thing in your file cabinet? Scan and toss, or shred if it contains sensitive data like a Social Security number.

Digital storage has many upsides. You don’t have to pay much attention to space restrictions as you would with physical files. Also, it’s easier to securely share and keep items, and you can search for files by dates or keywords.

Some fancy scanners such as the ScanSnap automatically sort documents based on file type (photo versus receipt) and name files based on scanned content. If you don’t have the budget or room for another machine, a smartphone app is a handy alternative.

One last essential tool: a service for storing and syncing your digital data in the cloud, so you don’t lose everything if your computer is stolen or damaged. Which one you choose will depend on what features are most important to you, but popular services include Dropbox, Google Drive and iCloud.

It’s also smart to take advantage of any proprietary storage features your financial advisor may offer, which allow you to securely store and share financial data with each other, as well as trusted family members, and helps them coordinate with other professionals (such as your accountant at tax time).

Think like an executor

The most crucial papers to organize are the ones those closest to you will need when you’re no longer around. This includes your will, bank statements, insurance policies and birth certificate, for starters. So put yourself in your executor’s shoes when storing estate paperwork – this kind of planning is about helping others.

Online services that organize and store all your vital details in a single convenient place are the latest innovation on this front. Some, such as Everplans, will even walk you through making a plan for everything from funeral details to healthcare wishes, sort of like TurboTax for end-of-life planning. You could also use an off-the-shelf workbook such as “The LastingMatters Organizer” to document your wishes.

As for notarized physical documents, storing them in a fireproof safe makes sense for most. Be sure your family knows where the safe itself is, how to get into it and what they can expect to find inside. You can also keep an extra copy in a safe deposit box or with your estate attorney.

Know what to keep

Certain official records deserve physical safekeeping: passports, Social Security cards, birth certificates and adoption decrees, property and vehicle deeds, marriage certificates, divorce decrees, signed and notarized powers of attorney, a will and medical directive paperwork. While you can pay to get another copy of many of these, it’s better to have them and not need them than the opposite.

Design a breadcrumb trail

This tip is especially relevant for worst-case-scenario documents such as your medical directive. Experts recommend keeping a copy in your car’s glove box, as well as giving copies to your doctor and your preferred healthcare proxy. You can then list these as “in case of emergency” or ICE contacts on a card in your wallet and in your smartphone’s emergency call screen (for iPhone users, add this data in Apple Health; Android users can go to Settings > About phone > Emergency information).

Don’t forget about digital access that your loved ones will one day need, which means everything from email and bank accounts to photo and music sites. Few of us think to create a paper trail to help locate these accounts and login IDs because it might invite unauthorized access. However, there is a secure way to guide your heirs.

The first step is to make an inventory. Next, document the details in a safe place. You can use a secure spreadsheet template to get started at yourdigitalafterlife.com or you can use a service like LastPass, which has an emergency access feature that allows you to hand down passwords to heirs who can then securely maintain or close your accounts based on your wishes. If it’s your main household responsibility to pay the bills and keep tabs on financial accounts, we’re talking to you. You want to leave a legacy – not a logistical headache.

Create a command station

Productivity pros say every home office needs a central collection spot for notes, bills, reminders, paperwork and actionable items. To make this a working system, you’ll have to regularly plow through it all, whether daily or weekly. This will help free your mind to focus on the given task at hand, knowing your household has a system for tackling all the incoming paper.

Progress, not perfection

If your home office is a wreck right now, start small. Pick one tip that speaks to your specific situation and take action. What feels like a small win today could make a major, lasting difference for your loved ones.

If you’re still feeling overwhelmed, you can seek out a professional organizer or turn to your advisor. They know your financial situation and can help you focus on the record-keeping tasks that are important for your life.

Sources: Real Simple; pcmag.com; “Getting Things Done: The Art of Stress-Free Productivity;" LastPass; yourdigitalafterlife.com; Everplans; NPR’s Life Kit; keepitsafe.com

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.

What’s Your Money Mindset

What’s Your Money Mindset

Understanding your motivators can help you better control your wealth journey.

Sensible about dollars and cents? More carefree than careful? Planner or play-it-by-ear? Your money personality affects more than just your portfolio, it likely affects your relationships, too – with your spouse, your siblings and your children. Money means different things to different people, and it’s vital to have a conversation about your spending, investing and saving habits so that you and your family will be on the same page.

According to financial psychologist Dr. Brad Klontz, “We have beliefs clunking around in our heads, and for many of us, they’ve been passed down from our parents.” But if we take the time to dig into our partners’ attitudes as well as our own, we may be able to better appreciate what drives financial decisions, recognize roadblocks and make meaningful progress toward our shared goals.

While there are a few broad stereotypes, only you, your family and your advisor will truly understand your motivations. You may not fit squarely into any of these boxes, but you may recognize a few of your own traits or those of your loved ones somewhere in the mix.

The rookie

You’re thrifty and idealistic – and you’re likely saddled with student debt as you try to launch a rewarding career. You’re optimistic and hope to align your personal and professional lives with the values you hold dear. You’re not likely to be a big spender, but when you do spend, it’s on memory-making experiences like vacations.

Bottom line: You’re just starting out and might fear an unpredictable market. While understanding your risk tolerance is essential to investing well, remember that you need some risk to grow wealth. Fortunately, you’ve got time on your side as well as the power of compounding. Use both to your advantage.

The forward thinker

You’re a little older with an established career. You’re buying houses, having children, aiming for that corner office. You’re busy and earning more than ever, but most of your money may already be spoken for, earmarked for retirement or a child’s education. You’ve got more money than time, and varying priorities compete for attention.

Bottom line: It’s a struggle to find time to dig into your investments and manage everyday expenses as well as your emergency savings. You prefer to delegate some of those decisions to an advisor, offering input along the way.

The influencer

You work hard and play harder. You’re always hustling so you can enjoy the finer things in life. You drive a nice car, carry the latest phone and eat Instagram-worthy meals. For you, your self-worth is tied to your net worth. You believe there’s no such thing as too much money, and you splurge regularly.

Bottom line: For you, a budget may not seem exciting, but it’s a way of holding up a mirror to overspending and staving off debt. You may not enjoy sharing control over financial decisions with someone else, but a trusted source can serve as a guardrail to get you closer to your long-term goals.

The ostrich

An ostrich sticks its head in the proverbial sand and avoids thinking about money. You’re not quite sure how much you have, what you spend or what you owe. And you may feel overwhelmed when it comes to financial details.

Bottom line: Ignoring your finances could mean missing out on an employer’s 401(k) match or not understanding your household expenses should you ever need to take over. If you find money management complicated or cumbersome, rely on your advisor and automate other aspects, like bill paying or contributing to your 401(k).

The stockpiler

You watch every penny, prioritizing saving and frugality. The goal is to have more money than you need, which gives you a feeling of safety and control. You may also feel uncomfortable talking about money, even with those closest to you. If you’re tired of worrying about money, you may want to assign more of the daily details to your advisor, who can shoulder some of the responsibility.

Bottom line: Saving is a wonderful habit, but if you sock most of your money away in cash and conservative investments, you may be too risk averse. Strike a balance to help you reach your short- and long-term financial goals and enjoy the journey.

The scout

The scout is well-prepared for the long haul. You see money as a tool and are willing to use it to achieve your goals. You understand that not everything will go your way, but you’re cautiously optimistic that a long-term plan will eventually get you where you want to go – no matter what is happening in the headlines.

Bottom line: You manage money with both your head and your heart, relying on expert advice when you need it. Be sure to build a trustworthy team of professionals, including an accountant and estate planning attorney, to ensure you maintain balance in all aspects of your financial life.

Planning for your financial future, like climbing a mountain, is a journey that each of us approaches a little differently depending on what we hope to achieve, our time horizon and our willingness to take on risk at that particular moment. The one thing we all have in common is the need for a guide to help us forge a path to prosperity.

Next steps

Level up your financial prowess by:

- Being honest about your financial tendencies and identifying habits

- Talking to your family about what your shared financial goals look like

- Speaking to your advisor to determine how you can achieve your dreams

Sources: ally.com; sofi.com; motleyfool.com; nerdwallet.com; investopedia.com; moneyharmony.com; empower.me; kiplinger.com; Raymond James research; University of Minnesota

All investments are subject to risk, including loss.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.