Archive for the ‘Newsletter’ Category

CrossleyShear Wealth Management's Media

25th Anniversary Gala

Save the Date 25th Anniversary Gala

October 28th | 6:15 pm–10:00 pm

Kennedy Space Center, Atlantis venue

Join us under the space shuttle Atlantis as we celebrate our success over the past 25 years. We couldn’t have made it this far without you! The festivities will include dinner, drinks, live music and dancing, too!

* Invitations will be sent six weeks prior to event with a link to RSVP. Dress will be black tie optional.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.

From the Desk of Dale Crossley and Evan Shear

From the Desk of Dale Crossley and Evan Shear

We hope you and your family are enjoying a relaxing summer. While there is still time to savor the rest of the season, this coming month marks preparations for a new school year and often prompts families to consider education expenses and planning. With the average cost of a four-year college degree approaching $150,000, we thought it would be helpful to share some helpful articles on education funding. As you review the many tax-free savings and estate planning benefits, there is no one-size-fits-all approach, so we can help you find the best options to suit your financial plan.

A popular education investment account is a 529 plan, a tax-advantaged investment account designed to help families save money for a child’s education. A recent update to the Secure 2.0 Act will soon provide an opportunity to revamp savings by allowing beneficiaries to make tax-free and penalty-free rollovers from 529 plans into a Roth IRA for a portion of the unused funds. This new law helps remove concerns about overfunding a 529 college savings account and ensures that families that save for their child’s education are not later penalized. This article offers important information on the eligibility and requirements of this provision in order to reposition money in a 529 plan in the event it isn't used for education.

Additionally, these education planning resources offer further valuable information on the benefits of a 529 plan, such as which education expenses qualify, how it compares to other savings strategies, and how it can be used as an estate planning tool. In addition, there’s an article on the benefits of using a securities-based line of credit (SBL) instead of student loans.

We hope you find these resources a helpful starting point to further discussions with your planner. Please feel free to contact us for guidance throughout this process and for help examining which options best align with your needs and goals.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.

There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. All opinions are as of this date and are subject to change without notice. Past performance is not a guarantee of future results.

Raymond James does not provide tax or legal services. As with other investments, there are generally fees and expenses associated with participation in a 529 plan. There is also a risk that these plans may lose money or not perform well enough to cover college costs as anticipated. Most states offer their own 529 programs, which may provide advantages and benefits exclusively for their residents. Investors should consider, before investing, whether the investor’s or the designated beneficiary’s home state offers any tax or other benefits that are only available for investment in such state’s 529 college savings plan. Such benefits include financial aid, scholarship funds and protection from creditors. The tax implications can vary significantly from state to state.

From the Desk of Dale Crossley and Evan Shear

From the Desk of Dale Crossley and Evan Shear

We hope this edition of The Journey finds you and your loved ones well. In light of the calls received over the past several months about the economy and market conditions, we thought it would be helpful to address a few frequently asked questions below. As always, please don’t hesitate to contact us if you have additional questions or needs. We’re always here to help.

Frequently Asked Questions

Question 1: When will we know the market is improving? Is the market improving?

The rainbow appears before the end of the storm. Generally, a bear market is already doing better before good news hits investors. Bear markets follow a pattern and it’s not always easy to identify what stage we’re in.

1. What’s going on? The first indications of a bear market are generally passed off as a bad day or week in the markets. Most investors understand the markets frequently rise and fall and reacting every time the markets dip is futile. Some investors try to take advantage of “bargains” at this time.

2. Bear market! Eventually, it’s obvious a market dip wasn’t just a bad week or few weeks. Panic tends to set in. At this stage, investors realize that taking advantage of “bargains” led to further losses, and the markets won’t rebound until the cause of the crash is no longer an issue.

3. The long haul. After stock prices begin to stabilize, investors recognize that losses will not be recouped overnight. Glimmers of hope occur on occasion, but then optimism is quickly lost. This is the longest period of the bear market, usually lasting several months.

4. The end. Almost nobody recognizes the end of the bear market until after it’s over and stocks are already well into their recovery. So, the rainbow appears before the end of the storm. We just need to find it!

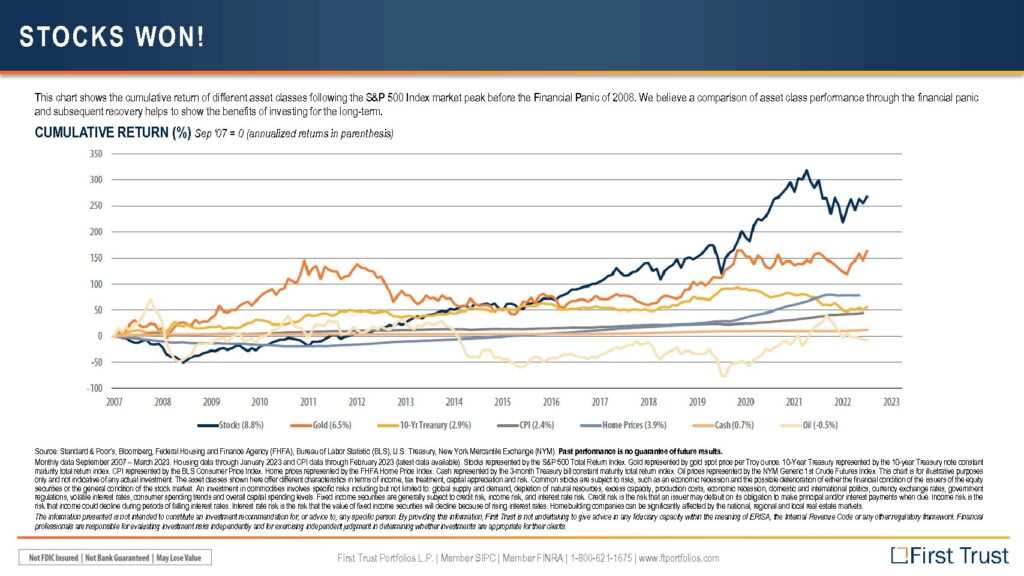

Question 2: Am I better off investing in the stock market when it periodically crashes?

The chart below might help you breathe a little easier as we remain in stage 3 or 4 of a bull market. The chart demonstrates how the S & P since 2007 has outperformed all other types of investments in annualized returns by far, including gold, 10-year treasury note and real estate. Hopefully, this chart provides some welcome perspective and demonstrates the importance of investing for the long term.

Question 3: Is the U.S. dollar going to be replaced as the global currency?

As Michael Lebowitz states in his recent article, The Dollars Death? Not So Fast - Part One, “The old saying goes that the U.S. dollar is the cleanest shirt in the dirty laundry.” There are other currencies out there, but they are simply not suitable at this time. Rumors are plentiful that some other currency is ripe to take the place of the U.S. dollar, particularly the Chinese yuan or bitcoin. Since 1250, the world has used eight different global currencies, with a relatively short history for the U.S. dollar’s reign. The demise of each previous currency came about due to financial mismanagement. Although the U.S. dollar is certainly less stable, due to in large part our amassing trillions in debt, there’s currently no better replacement. Here’s a link to Michael Leibowitz’s full article so you can learn more and view several insightful charts and graphs.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.

There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. All opinions are as of this date and are subject to change without notice. Past performance is not a guarantee of future results.

Document Shredding and Food drive

Document shredding and food drive

Clean out your cabinets and drawers of those old documents and bring them to be safely shredded, on site, by the professionals of Shred it™

and enjoy some good food and live music!

When: May 6th

Where: Outside of the Merritt Island office 2395 N. Courtenay Parkway

Time: 11:00am-2:00pm

Please consider bringing a non-perishable food item for our Food Drive to benefit Harvest Time International

Please Donate:

Low sodium canned vegetables - Canned meats - Canned soups - Boxed oatmeal or grits - Canola or olive oil - Peanut butter - Nuts - No sugar added fruit cups - Canned beans - Granola/Protein bars - Pasta - Beans - Rice - Dry powdered milk

Questions please contact

Karin@crossleyshear.com or call 321-452-0061

Raymond James is not affiliated with Harvest Time International, Shred-it, or 4th Street Fillin Station.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.

Make data privacy a priority in 2023

Make data privacy a priority in 2023

As our lives become more digitally integrated, our data becomes more valuable.

Often, data collectors say that the vast amount of information they take in is tightly secured or anonymized before it is packaged and resold. However, MIT researchers discovered in 2018 that individuals could be identified by combining two anonymized data sets covering the same population. A 2019 series from The New York Times went further, exposing the risk to privacy on a massive scale if a major tech firm’s anonymized location data was stolen and cross-referenced to publicly available property records.

As long as consumers’ concerns about privacy remain limited, there is little incentive for companies to cull their data collecting habits. When buying a new smart device such as a phone, tablet or computer or using a new service, look into its commitment to privacy. The market for such devices is growing, but at the moment they tend to be on the premium side of the product spectrum. Expect that to change as this topic gains traction.

In the meantime, here are some best practices to help minimize the amount of your information that data collectors can access.

Turn off personalized ads

Many of the largest ad space sellers, particularly those providing tech services like email and social media, now give the option to depersonalize your advertising experience. They’ll still collect the information, but there are some limits to how specifically targeted the ads can be. This is becoming a battleground topic in the tech industry, as companies that don’t rely on ad sales are finding privacy to be a strong selling point.

Skip the quiz

That silly online quiz to help you determine which fast food mascot you are may be mining serious information about you. Though it’s a bad practice, many online accounts rely on security questions to establish your identity, questions that are easily snuck into online quizzes.

Go digital and shred the rest

Your home or driveway may be advertising your wealth, making your mailbox and your trash a target. Despite the well-publicized thefts of user data in recent years, an online account is in many ways more secure than an unlocked mailbox, and generally less personal. Privacy experts recommend making the switch, and when you do get mail that contains information about your health, finances or family, make sure to shred it before you toss it.

Know what health data is being collected

The Health Insurance Portability and Accountability Act, or HIPAA, protects the information shared with your care provider. There is no similar regulation for health data you share with your fitness device manufacturer. It’s worth your while to make sure you understand what information is being collected and for what purposes. Go into the device settings to see what options you have. The EULA, or end-user license agreement, will have more information if you can read legalese.

Sources: The New York Times; Vox; The Washington Post; Fast Company; Massachusetts Institute of Technology; Consumer Reports; NPR; Goldman Sachs; ZDNet.com

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.