Archive for the ‘Newsletter’ Category

CrossleyShear Wealth Management's Media

From the Desk of Dale Crossley and Evan Shear

From the Desk of Dale Crossley and Evan Shear

“In a Blink of an Eye”

It seems like all of our lives have been drastically altered in the blink of an eye. Not that anyone needs a reminder of what we have all been going through, but from a market standpoint, we hit a high on 2/19 and then within a few weeks we were deep in a bear market for the first time in over 10 years. From a low of around 30% down for the year, the markets have tried to find some footing as of the writing of this article. It will take some time for our economy to heal, but we are certain it will.

More importantly, our lives and how we live has changed. For us personally, we have been working remotely since early on in this pandemic. Our homes and home offices have become our war rooms and our trading floors. We have done numerous Zoom meetings and even Dale, who admittedly isn’t the best with technology, has become more proficient with it. My kids are all home and my oldest son’s sophomore college baseball season came to an abrupt end. The shining light of this new lifestyle is the nightly family meals and marathon UNO games. I’ve been trying to look for the joy in this crisis and family and friends, including our clients, have definitely been the best part. We have heard from many of you checking in with us, not just to see how your portfolios are doing, but rather how WE are doing. We want you to know that these calls and notes have a special place in the hearts of our entire team.

This is certainly not the crisis any of us foresaw when we started discussing the possibility of a coming recession or market volatility. For the most part we have weathered it rather well with our tactical models and time-tested strategies. Having a plan and sticking with it is vital when times of stress hit us, both financially and personally. It’s when we allow emotions to take over that we have seen the most destruction to wealth – not only today, but in the past. We appreciate the faith and trust you have all given to Dale, myself and the entire firm and hope you realize how special you are all to us.

Take care,

Evan

As Evan mentioned, emotional financial decisions are rarely helpful and often devastating. This has been a very trying time for us all, but also very interesting. As a student of behavioral finance every day provides an opportunity to learn. Within minutes we can receive completely opposite questions or concerns from clients, sometimes it might even be the same person. "Should we be going to cash to stop the bleeding?” "Should we be buying to take advantage of the downturn?" More than anything we are thankful that you have all entrusted us to answer these questions for you and your families. We are humbled to be able to lead, guide and direct you.

We certainly don't have all the answers, but our commitment has and will always be to put your interests above our own. In an effort to do that, we will continue to separate the narrative from the data and do the requisite research and continuing education to ensure that we are giving the best possible advice to keep you on track to reach your goals. That is the promise of our entire team.

The markets will recover, because they ALWAYS do. They will start the recovery before the news says, “all clear.” Our country will recover, because it ALWAYS does. That doesn't mean perfect. It will never be perfect. Don't bet against our Country. Don't bet against our scientists, our doctors and healthcare workers, our entrepreneurs, our philanthropists, or our people.

We encourage you to take what extra time this tragedy has afforded you to reexamine what's truly important to you. I am thankful for being able to use this time to reconnect with family and friends, even if mostly remotely. Reach out and check on people. Let your loved ones know how you feel. Reexamine your health plan, diet and fitness. Read a book. Take a walk. Finish a project. Learn something new.

This has no doubt been a roller coaster ride and will continue to be for the near future. Unfortunately, it’s only the scary part of the ride, without any of the fun. Do your best to separate the narrative from the data. This may mean turning off the TV for a few days. Everyone please take care of yourself and your family. Many things have changed forever, but we will recover and be stronger than ever. This too shall pass.

Take care,

Dale

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.

Reinvesting in a rising market is like merging into traffic it’s best to have a plan

Reinvesting in a Rising Market is Like Merging into Traffic... It’s Best to Have a Plan

Getting Out of the Market is Easy... Getting Back in can be Another Matter Entirely

Investors are regularly inundated with scary headlines and dour forecasts that provide ample reasons to get out of the stock market. COVID-19 has been just that kind of catalyst. Combine that with a human’s natural ‘fight or flight’ instincts that kick-in when markets are volatile, and it is not unusual to find oneself holding too much cash after a big sell-off. Unfortunately, we believe few that find themselves in this position know what to do or have a plan for reinvestment. This week’s edition of the Weekly View is dedicated to the age-old question: ‘What do I do when I have too much cash on the sidelines?’

FIRST: SWALLOW YOUR PRIDE

It is easy to celebrate successes; we believe that the best investors are those who know how to manage their mistakes. No one likes to admit that that they bought or sold for the wrong reasons, or that their hopes or worries were misguided. Many would prefer to stick with their decisions, even when the preponderance of evidence suggests otherwise. We believe investors need to get comfortable with the notion of ‘being wrong’ and moving on. If you sold stocks and the market did not go down, don’t beat yourself up over it. It is important not to compound a bad decision by failing to recognize when the facts change. In our view, ‘being wrong’ happens to all investors from time to time, but ‘staying wrong’ often makes the difference between investment success and failure.

SECOND: DETERMINE WHETHER THE CONDITIONS HAVE CHANGED

If you sold stocks in 2020 because of COVID-19, it is important to recognize that the market will likely bottom well before macro-economic conditions improve. While no one can say for certain when the crisis will be behind us, we do recognize that a significant amount of ‘bad news’ may already be discounted into stock prices and an unprecedented amount of monetary and fiscal stimulus has already been implemented. For example, the Federal Reserve has lowered the Fed Funds Target Rate to 0%, restarted quantitative easing, and implemented large lending facilities to support market functioning. Congress has also passed the Coronavirus Aid, Relief, and Economic Security Act (CARES), which is the largest fiscal stimulus program in US history valued at $2.2 trillion. Monetary and fiscal policymakers across the globe have also enacted similar stimulus programs. According to Evercore ISI, nearly 300 stimulus measures have been announced in the past month around the world.

THIRD: DETERMINE IF CASH UNDERMINES LONG-TERM GOALS

In today’s low interest rate environment, large cash holdings could be an obstacle to funding future obligations, such as college or retirement. There is also a chance that long-term inflation rates rise with increased quantitative easing (QE) and generous fiscal stimulus programs; ultimately eroding purchasing power. When cash is accumulating to a reasonable level of interest in the bank or in a brokerage account, the long-term costs of sitting out can be less punitive. However, with short-term rates below inflation, cash on the sidelines provides negative real returns as it sits idle. If one needs their portfolio to grow, less risk-taking today could lead to greater risk taking tomorrow.

FOURTH: DON’T BE ‘PENNY-WISE AND POUND-FOOLISH’

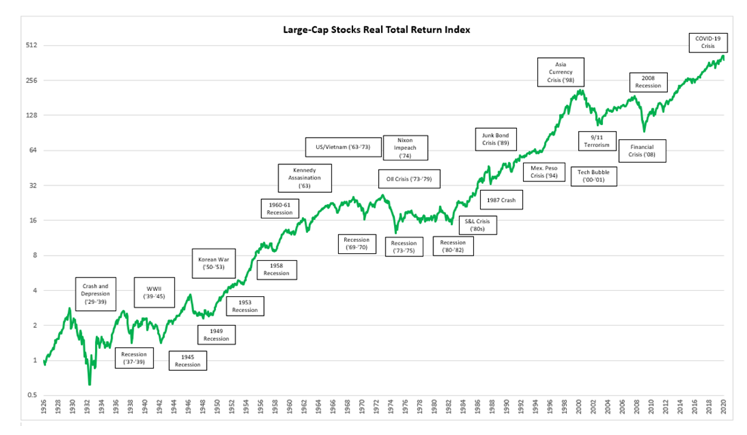

In our view, the longer an investor’s time horizon, the less important market entry points are. We believe the adage that successful investing is about ‘time in the market,’ NOT ‘timing the market’ holds merit for long-term investors for two reasons. First, over long-time horizons, the US stock market generally recovers its losses and continues to climb the ‘Wall of Worry’ (chart below).

Source: IFR, Wikipedia, RiverFront, CRSP, Data updated through February 2020. Shown for illustrative purposes and not intended as an investment recommendation. Not indicative of RiverFront portfolio performance. Past performance is no guarantee of future results.

Second, long-term investors benefit from a powerful force: compound interest. Compound interest allows a $100 investment growing at 10% annually to return more than 6 times an investor’s initial money after 20 years. We believe that investors who jump in and out of the market with significant amounts of their portfolios tend to be un-invested or underinvested more frequently and thus less likely to experience the full benefits of market recoveries or compound growth.

FIFTH: DEVELOP AND EXECUTE ON A PLAN

Second, long-term investors benefit from a powerful force: compound interest. Compound interest allows a $100 investment growing at 10% annually to return more than 6 times an investor’s initial money after 20 years. We believe that investors who jump in and out of the market with significant amounts of their portfolios tend to be un-invested or underinvested more frequently and thus less likely to experience the full benefits of market recoveries or compound growth.

This is a critical part of our process at RiverFront. There are many reinvestment strategies that have shown historical efficacy. We believe that entry and exit strategies should be consistent with the investor’s goals and objectives and not solely dependent on one’s ability to accurately forecast market movements over short periods of time. Thus, when you deviate from your long-term goals, we think it is critical to have a plan for how you are going to return to them.

A REINVESTMENT PLAN: MERGING INTO TRAFFIC

Reinvesting into a market that could be rising can be similar to an activity that we are all familiar with: merging into moving traffic. For most of us, the action of merging requires little thought because it has become second nature. However, if we take a minute to examine it, we can identify three important steps that can be applied to the reinvestment process.

Get Started: When you are merging onto the interstate you start the process immediately by getting up to speed. You don’t stop on the entrance ramp to wait for an opening because if you did you would lose all of your momentum (and your nerve). Likewise, when reinvesting cash, we believe investors should also start the process sooner rather than later. We believe that stocks will generally be higher than current levels 12-18 months from now. Therefore, we recommend that long-term investors with time horizons greater than 5 years, begin putting some of their excess cash to work as soon as possible. In the current market sell-off, we are concerned about slower earnings growth in the quarters ahead, but we believe that the market will likely look through those earnings once there are increasing signs that the world is getting COVID-19 under control.

Shown for illustrative purposes. Not indicative of RiverFront portfolio performance. Past performance is no guarantee of future results.

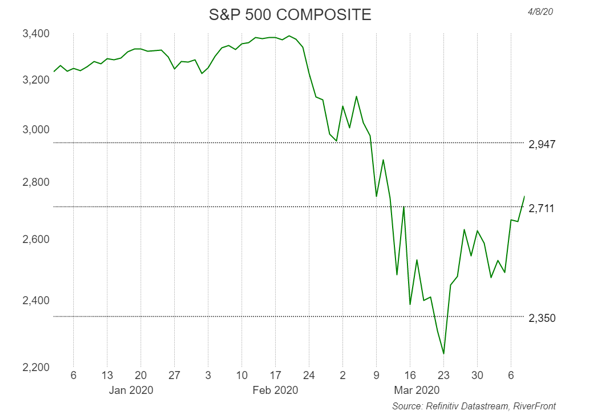

- PORTFOLIO IMPLICATIONS: Reinvest some Opportunistically: When merging onto the highway, gaps in the traffic will appear as you get up to speed. These gaps provide opportunities to merge more quickly. From a reinvestment perspective, investors can designate a portion of their cash to take advantage of opportunities that may arise as a result of market volatility. In fact, after more than a 20% bounce from the March 2020 lows, it would be surprising if we did not experience some pullback or digestion period in coming months. Should that occur, some investors may want to accelerate their purchases, taking advantage of that weakness. Even so, at or around the 2350 level on the S&P 500 might be an attractive opportunistic entry point. Others may want greater evidence that the COVID-19 crisis is behind us and therefore prefer to be opportunistic ‘on strength.’ We believe that the market may be putting virus fears behind it if the S&P 500 holds and eclipses important resistance levels like 2711 and 2947.

- Complete Gradually: Gradually the merger lane comes to an end, and the driver must complete the merge. Reinvestment windows also come to an end because investors risk missing out on the ‘power of compound interest’ if they fail to reinvest in a timely manner. To offset the risk of bad timing, investors can use a dollar-cost- average approach to gradually reinvest on a series of dates over a defined time period. Three to six months is probably the appropriate time period for a long-term investor to complete their cash reinvestment period, in our view.

RiverFront’s balanced portfolios are currently positioned slightly defensively as the portfolio’s equity weightings are 3-6% below their composite benchmarks. Our portfolio management teams continue to monitor COVID-19 developments and meet regularly to construct and implement de-risking and re-risking plans.

Source: https://www.riverfrontig.com/resources/commentaries/single/weekly-view-reinvesting-rising-market-merging-trafficits-best-have-plan/

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Past results are no guarantee of future results and no representation is made that a client will or is likely to achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Information or data shown or used in this material is for illustrative purposes only and was received from sources believed to be reliable, but accuracy is not guaranteed.

In a rising interest rate environment, the value of fixed-income securities generally declines.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios. For more information on our other portfolios, please visit or contact your Financial Advisor.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

You cannot invest directly in an index.

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

Market Cap index information calculated based on data from CRSP 1925 US Indices Database ©2016 Center for Research in Security Prices (CRSP®), Booth School of Business, The University of Chicago.

Used as a source for cap-based portfolio research appearing in publications, and by practitioners for benchmarking, the CRSP Cap-Based Portfolio Indices Product data tracks micro, small, mid- and large-cap stocks on monthly and quarterly frequencies. This product is used to track and analyze performance differentials between size-relative portfolios.

ranks all NYSE companies by market capitalization and divides them into ten equally populated portfolios. Alternext and NASDAQ stocks are then placed into the deciles determined by the NYSE breakpoints, based on market capitalization. The series of 10 indices are identified as CRSP 1 through CRSP 10, where CRSP 10 has the largest population and smallest market-capitalization. CRSP portfolios 1-2 represent large cap stocks, portfolios 3-5 represent mid-caps and portfolios 6-10 represent small caps.

Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2020 RiverFront Investment Group. All Rights Reserved. ID 1149365

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.

ESPN scrambling to figure out programming while live sports shut down indefinitely

ESPN scrambling to figure out programming while live sports shut down indefinitely

Disney’s ESPN has long called itself the worldwide leader in sports. Now it will have to figure out what to do when there aren’t any.

On what could be called Black Thursday for major sports leagues, Major League Baseball and the National Hockey League suspended play, following the National Basketball Association’s lead on Wednesday. The National Collegiate Athletic Association followed by canceling March Madness, the annual men’s and women’s basketball tournaments that crown national champions, and all other winter and spring championships including the Frozen Four and the College World Series. The PGA Tour canceled the Players Championship after the first round and all subsequent tournaments until the Masters, which has also been postponed. Major League Soccer announced it is suspending play for 30 days.

That leaves all-sports networks -- particularly ESPN, which owns more rights to live games than any other media entity -- with several unprecedented problems.

Most urgently, ESPN will need to broadcast replacement programming for the games that won’t be happening. In the near term, that includes NCAA conference championship games, NBA games and first-round NCAA women’s basketball tournament games. Beyond that, ESPN has additional live college sports on ESPN+, its streaming service, and other linear networks including ESPN2, ESPNU and ESPN3.

Extended cancellations of live sports is not only bad for ESPN, but for the entire traditional pay-TV business.

With millions of Americans already leaving cable for streaming services each year, losing live sports for months may convince a surge of new defectors to try life without cable, which typically costs between $60 and $100 per month -- and some are likely not to return even when sports come back. Disney makes about $11 billion annually from ESPN and its sister networks, between getting about $9 per month for all the ESPN networks in affiliate fees and earning about $2.75 billion in yearly advertising, according to research firm LightShed. ESPN has about 81 million subscribers, LightShed estimates.

How ESPN could fill the gap

ESPN executives are urgently discussing plans to fill air time, according to people familiar with the matter. With news still fresh about coronavirus cancellations, it’s likely ESPN will stick with hourly editions of SportsCenter, the network’s flagship live sports studio show, to fill gaps in the near term to update audiences on the ramifications of the coronavirus. ESPN will air SportsCenter from 5 p.m. ET until midnight on Friday, following “Get Up” live at 2 p.m. ET and “First Take” at 4 p.m. ET.

Next week, ESPN will get another shot in the arm of breaking sports news with the likely start of National Football League free agency, which will provide fresh material for several weeks. Free agency officially begins Wednesday, though deal news often starts to leak on Monday, when so-called legal tampering kicks off -- though even those dates are contingent on NFL players approving their new collective bargaining agreement on Saturday.

“We have great relationships with our league partners and are confident we can address all issues constructively going forward,” an ESPN spokesman said in a statement. “We are working closely with our partners during this unprecedented situation. Our immediate focus is on everyone’s safety and well-being.”

If games are canceled for a number of weeks or months, ESPN may be forced to get creative. Here are some potential options beyond SportsCenter and the network’s regularly scheduled studio shows, which may run dry of news and “hot takes” if cancellations drag on:

- “30 for 30” documentaries: ESPN has produced 88 “30 for 30” sports documentaries, all of which are available on demand with an ESPN+ subscription. ESPN has previously aired the documentaries to fill time when games are postponed due to weather.

- Esports: Live streams of video gamers competing have drawn millions of viewers on Amazon’s Twitch and would be a rare example of live programming that could go on during a widespread coronavirus quarantine, as players could compete at home or without live audiences. Pete Vlastelica, CEO of Activision Blizzard Esports, tweeted Wednesday that matches would continue, though events would be canceled. Activision Blizzard owns the Overwatch League and Call of Duty League, which feature professional esports players and tournaments.“Given that nearly every major sporting event is currently cancelled or on hold with the exception of the UFC, I think it’s very possible we see game developers who have the biggest esports titles such as Activision Blizzard, Riot (League of Legends), Epic (Fortnite, Rocket League), and Valve (Counter-Strike, Dota) initiate discussions with major media organizations like ESPN and Turner, who have already broadcasted esports before,” said Rod Breslau, an esports journalist and consultant.

- Ad hoc programming: ESPN could develop new interview shows with on-hiatus athletes and coaches and will likely work with professional sports leagues to create new content as replacement programming.

- Library content: Longtime ESPN viewers may remember enjoying afternoon programming of “World’s Strongest Man” competitions or

- “Home Run Derby” from 1959 featuring Willie Mays, Ernie Banks, Mickey Mantle and others. ESPN could tap programming from ESPN Classic, which has been dropped as a linear network by most major pay-TV providers.

- Reruns of classic games: ESPN owns the rights to thousands of classic games in many sports and could choose to air games with new or live commentary from players and coaches who participated in the events.

However ESPN decides to fill air time, nothing like this -- entire leagues canceled for weeks or potentially months -- has ever happened before in the network’s history. The unprecedented turn of events will be a test for President Jimmy Pitaro, just two years into his job, and new Disney CEO Bob Chapek, who took the position less than a month ago.

Disney is also closing its theme parks, including Disney World and Disneyland in the U.S., for the remainder of March. The company will have to hope that Disney+, its on-demand streaming service, will pick up millions of new subscribers with parents and kids stuck at home under quarantine, to blunt the impending loss of revenue in what will almost certainly be a rough first and second quarter of 2020.

Source: CNBC, March 13, 2020. prepared by Alex Sherman

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.

Low Carb Chicken Marsala with Zucchini Noodles

Low Carb Chicken Marsala with Zucchini Noodles

Ingredients

- Boneless Skinless Chicken Breasts (2)

- Shitake Mushrooms Chopped (1 cup)

- Half an Onion Chopped

- White Wine (1/2 cup)

- Chicken Broth (1/2 cup)

- 3 Large Zucchinis Spiralized (or store-bought zucchini noodles)

- Butter (3 tbsp)

- Cornstarch (1 tbsp)

- Salt & Pepper

Directions

- Heat 1 tbsp of butter in medium skillet. While butter melts, season chicken with Italian seasoning on both sides. Add chicken to skillet and cook until done.

- Set chicken aside and cover for later.

- In the same skillet used for the chicken, add one tbsp of butter and sauté mushrooms and onions for about 5 minutes

- While onions, mushrooms, and wine simmer, whisk chicken broth and cornstarch together in small bowl.

- Add chicken broth and cornstarch mixture and remaining butter to the skillet and bring to a boil. Reduce heat and simmer till sauce thickens.

- In the meantime, take spiralized zucchini noodles and sauté in separate skillet till cooked through. Add salt and pepper to taste.

- Once sauce is thickened, add the chicken back to the skillet and toss in sauce till warmed.

- Serve over zucchini noodles and pair with your favorite wine!

Recipe from Crossley house Quarantine dinner

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.

Tax Deadline Changed to July 15

TAX PLANNING

The IRS has extended the deadline for filing your 2019 income taxes. Learn more about this important change.

The Treasury Department and IRS have officially extended the deadline for filing your 2019 tax return to July 15, 2020, in response to the COVID-19 outbreak.

If you’re expecting to receive a refund, you should still consider filing your taxes ahead of the new deadline. However, for those with a large tax liability, the new deadline may provide some extra time to develop a thoughtful strategy for paying the taxes due.

Common questions

Do I still need to file taxes by April 15, 2020?

No – the new deadline for filing your taxes is July 15. However, if you’re expecting to receive a refund, you should consider filing sooner.

Does this apply to state income tax payment deadlines?

Not necessarily. The extension is for federal income tax purposes only, not state income tax. Please consult your tax professional for more details about your state’s policies, which may adjust as COVID-19 updates unfold.

What if I pay estimated quarterly tax payments?

This delay applies to you, too. You will have a payment deadline of July 15 instead of April 15.

What do I need to do to elect the deferral?

No special election needs to be made if you decide to delay. Any interest or penalty from the IRS from April 15 to July 15 will be waived. Penalties and interest will begin to accrue on any remaining unpaid balances as of July 16, 2020.

Does this mean I can make 2019 IRA contributions until July 15?

Yes. Per IRS publication 590-A: “Contributions can be made to your traditional IRA for a year at any time during the year or by the due date for filing your return for that year, not including extensions.” The due date for filing the 2019 return is now July 15, 2020, so you have until that date to make 2019 IRA contributions.

How can I learn more about this change?

The IRS has established a special section on their website to help taxpayers stay up to date with COVID-19-related changes. Visit irs.gov/coronavirus to explore related resources, and reach out to your tax professional and financial advisor with any questions you have about your specific tax situation and financial plan.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.