Should You File Early for Social Security?

Waiting until full retirement age makes sense for many investors – but not for every investor.

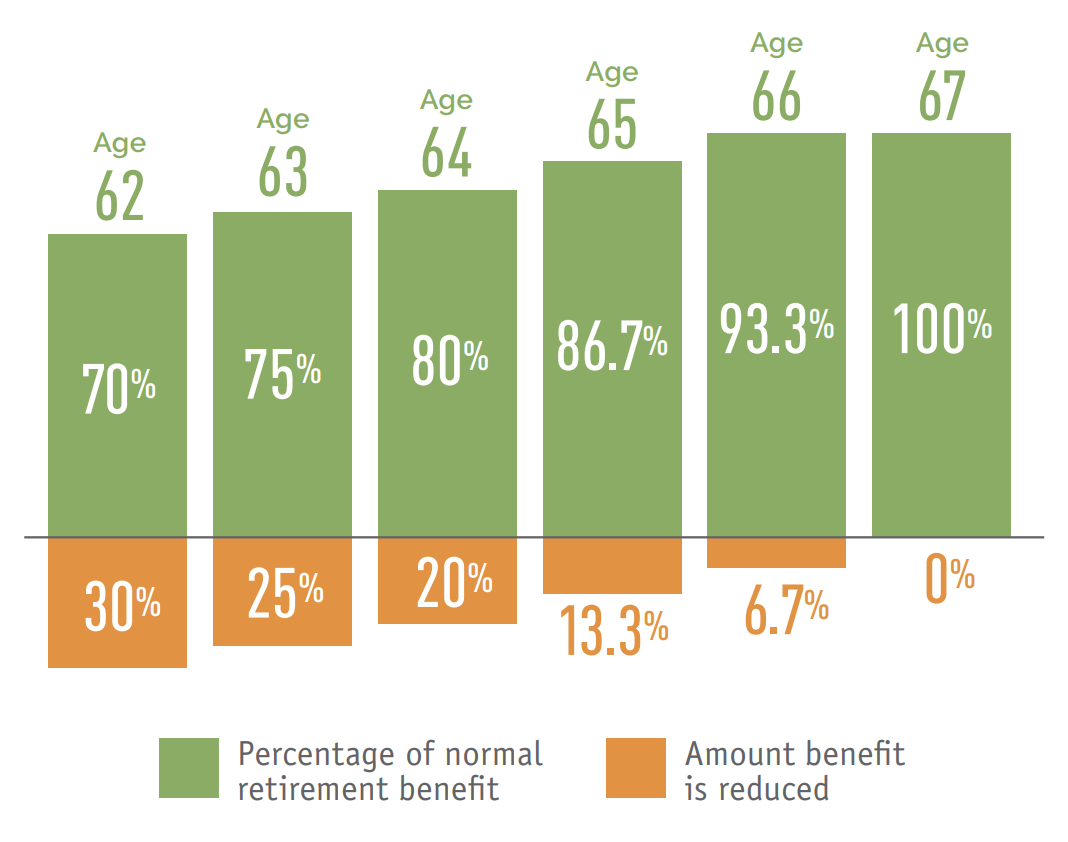

Conventional wisdom and a little bit of math tell us that waiting at least until full retirement age (between 66 and 67, depending on when you were born) will net a larger monthly payout than filing for Social Security as soon as you’re eligible at age 62. If you can wait even longer, you’ll get an 8% increase in your monthly benefits every year you delay between your full retirement age and age 70 – a potential 8% to 32% increase (a pretty impressive “rate of return” that’s hard to beat).

This assumes, of course, that you have good health as well as enough income and/or retirement savings that you can afford to wait.

But this approach may not fit every case. Depending on your financial standing, personal life expectancy and spousal situation, filing early can actually be advantageous. But make this decision carefully – remember, filing early yields a permanently reduced Social Security benefit.

Consider these three factors when deciding whether or not to file early:

Your cash needs

Sometimes, the best laid plans go awry. You may have to leave your job unexpectedly for health reasons – you may get burned out, or a business deal doesn’t go as well as hoped and you find yourself in debt. Perhaps you find yourself wanting – or needing – to spend more time with those you love. If you don’t have enough savings to retire sooner than planned, think about claiming Social Security benefits early.

Social Security offers a consistent source of income, so it can make for a great backup plan. But it’s important to really do the math and budget accordingly, since it’s unlikely to be a princely sum. Benefits are estimated to average $1,543 in January 2021, which would sum to about $18,516 per year. The maximum benefit at full retirement age for 2021 is $3,148, about $37,776 per year.

Some strong savers still like having extra income to fund more of their wants in early retirement, perhaps preferring to let dedicated retirement savings accounts continue to grow. The extra income can enhance the so-called “go-go” years, a period when we can expect to have the most time and energy when we first enter retirement.

Your health

If you live to the average life expectancy for someone your age, you’ll receive approximately the same amount over your lifetime whether you start collecting benefits sooner or later. But the math only works out if you live to your late 70s, the average American life expectancy. If you have a significant health event or have a family history of illness, filing early could be a smart option.

Your spouse

If you’re the lower-earning partner, your lifetime benefits will also be lower. Ask your advisor to calculate how to maximize your total household benefits. This plan could involve you filing earlier, and the higher-earning spouse delaying their more substantial benefits in order to get that 8% credit for each year between full retirement age and age 70. This strategy could maximize your benefits as a couple, and is also likely to secure higher survivor benefits for you when the time comes.

As with many financial decisions, the best Social Security claiming strategies need to account for your personal situation – your health, your savings, your marital status. Remember that you’re generally not eligible for Medicare until 65, so if you’re not covered by an employer, you may need to purchase your own health insurance coverage until Medicare kicks in.

It’s best to consult with your spouse and a knowledgeable financial advisor to help maximize this important source of recurring, inflation-adjusted and guaranteed income. Your advisor can help you run some calculations to maximize your household and lifetime Social Security benefits, which will help you and your spouse determine the most appropriate time to file.

Sources: Washington Post; Motley Fool; thebalance.com; cnbc.com; ssa.gov; Center for Retirement Research; investors.com

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Raymond James does not provide tax or legal services. Please discuss these matters with the appropriate professional.